How Does a Chargeback Work? A Step-by-Step Guide for Merchants (2026)

A clear, step-by-step explanation of how chargebacks work in 2026 — from the initial customer dispute through representment, arbitration, fees, timelines, and how to win.

If you accept credit or debit card payments, sooner or later a customer will call their bank instead of contacting you for a refund. That phone call kicks off a process called a chargeback — a forced reversal of the payment that pulls funds back out of your account, adds a fee, and gives you a short window to fight back with evidence.

Most merchants only learn how chargebacks work after their first one lands. By then, the deadline clock is already ticking and the money is already gone. This guide walks through the entire lifecycle — what triggers a chargeback, who's involved, what happens at each stage, how long you have to respond, what it costs, and how to tilt the odds of winning in your favor.

What is a chargeback?

A chargeback is a payment reversal initiated by a cardholder's bank (the issuing bank) on the cardholder's behalf. Instead of asking the merchant for a refund, the customer disputes the charge directly with their bank, and the bank pulls the funds back from the merchant through the card network.

Chargebacks were created in the 1970s as a consumer-protection mechanism under the U.S. Fair Credit Billing Act. The idea was simple: if a card was stolen, a product never arrived, or a merchant refused to issue a legitimate refund, the cardholder shouldn't be stuck with the bill. In 2026 the mechanism still works the same way — but it's used far more often, and roughly 60–80% of disputes filed against ecommerce merchants are now friendly fraud: legitimate buyers filing chargebacks instead of asking for a refund.

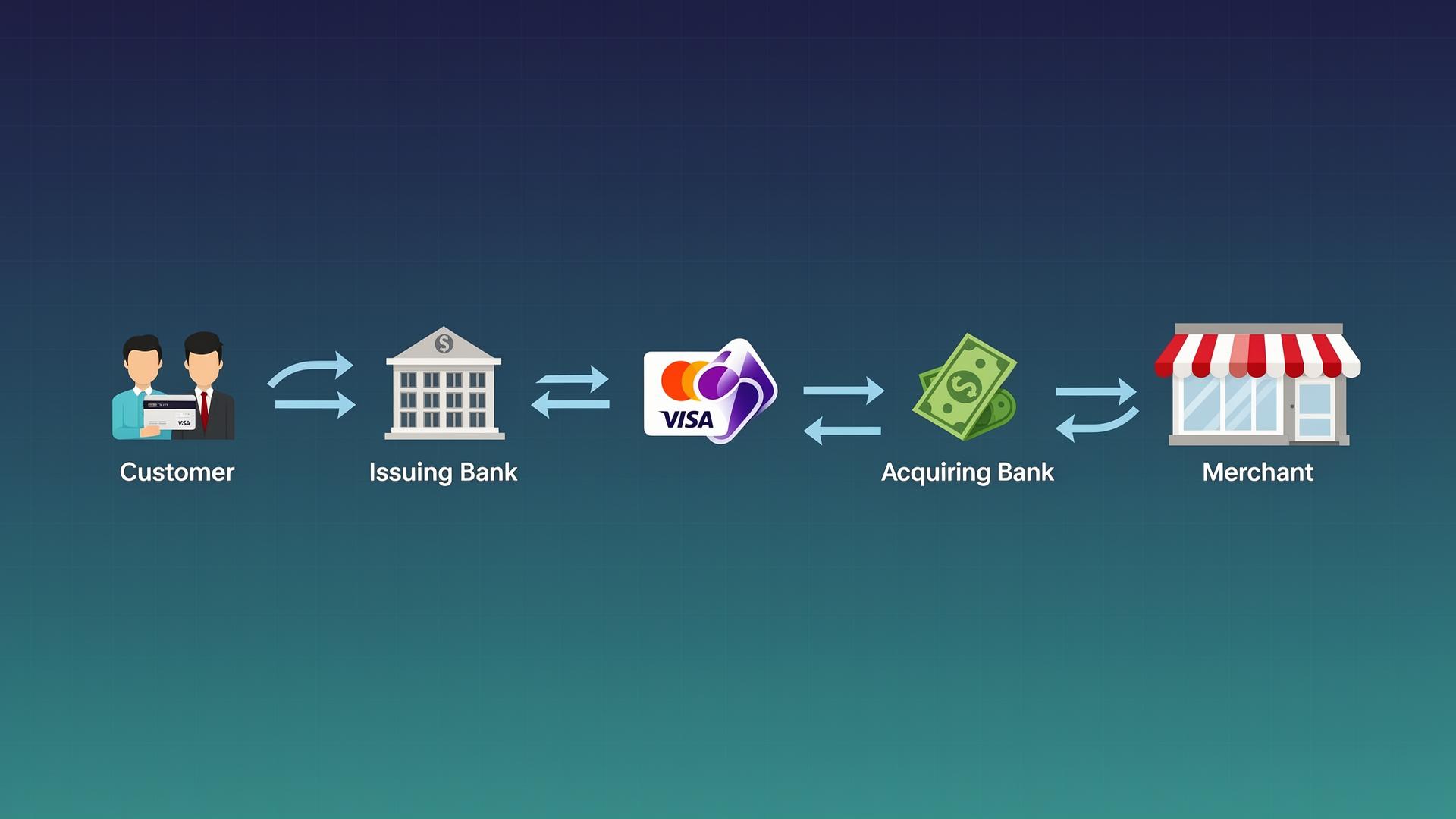

The five parties in every chargeback

Every chargeback touches the same five participants. Understanding who they are makes the rest of the process much easier to follow.

- Cardholder — the customer who made the purchase and is now disputing it.

- Issuing bank — the bank that issued the customer's card (Chase, Capital One, Barclays, etc.). The cardholder calls them to file the dispute.

- Card network — Visa, Mastercard, American Express, or Discover. They set the rules, route the dispute, and adjudicate if it escalates.

- Acquiring bank — the merchant's bank or payment processor (Stripe, Adyen, Braintree, and their underlying banks). They debit the merchant and forward responses back through the network.

- Merchant — your business. You receive the dispute notification and either accept the loss or fight it with evidence.

Money flows from cardholder → issuing bank → network → acquiring bank → merchant on the original purchase. On a chargeback, that flow reverses — and a fee gets tacked on at the merchant's end.

How a chargeback works, step by step

Here's the full lifecycle of a typical chargeback in 2026, from the customer's first call to final resolution.

Step 1 — The customer files a dispute

The cardholder contacts their issuing bank, usually through the bank's app or website, and disputes a specific transaction. They pick a reason code from a list provided by the bank — for example "product not received," "product not as described," "unauthorized transaction," or "duplicate charge."

In most cases the customer doesn't have to provide much evidence at this stage. The bank's job is to protect the cardholder first and investigate second.

Step 2 — The issuing bank reviews and provisionally credits the customer

The issuer takes a quick look at the dispute, decides whether it has merit on its face, and (for most reason codes) provisionally credits the customer's account within a few business days. From the customer's perspective, they have their money back almost immediately.

Step 3 — The chargeback is sent to the card network

The issuer files the chargeback through the card network (Visa, Mastercard, Amex, or Discover). The network applies the relevant reason code, attaches a deadline, and routes the dispute to the merchant's acquiring bank.

Step 4 — The acquiring bank debits the merchant

The acquirer pulls the disputed amount — plus a chargeback fee of typically $15 to $100 — out of the merchant's account. Stripe, Braintree, Adyen, PayPal, and others all do this automatically. The merchant sees the funds disappear before they've had a chance to respond.

This is the moment most merchants first learn a chargeback has been filed.

Step 5 — The merchant receives the dispute notification

The acquirer notifies the merchant with the transaction details, the reason code, the deadline to respond, and a request for evidence. Deadlines vary by network but typically fall between 7 and 30 calendar days from the date the dispute is filed — not the date the merchant sees it.

At this point the merchant has three choices:

- Accept the chargeback. The funds stay with the customer, the fee is forfeited, and the dispute closes. This is the right call when the customer is clearly right or the order value is below the cost of fighting.

- Refund the customer. In some networks (notably Visa under the VCR framework), issuing a refund after the chargeback is filed doesn't reverse the chargeback — but it can prevent the issue from escalating further on subscription products.

- Fight the chargeback with evidence. This is called representment.

Step 6 — The merchant submits representment

Representment is the merchant's formal response. The merchant assembles an evidence package — order details, shipping carrier and tracking, delivery proof, AVS/CVV match, IP and device fingerprint, prior customer messages, refund history, terms of service — and submits a rebuttal letter through the acquirer.

The evidence has to be specific to the reason code. A "product not received" dispute needs delivery confirmation; an "unauthorized transaction" dispute needs proof the cardholder authorized the purchase (AVS match, IP geolocation, login history, prior orders from the same account); a "product not as described" dispute needs the product description, photos, and any communication where the customer acknowledged the item.

The acquirer forwards the representment back through the network to the issuing bank.

Step 7 — The issuing bank reviews the evidence

The issuer evaluates the merchant's response against the cardholder's claim. If the evidence is compelling and the reason code is satisfied, the chargeback is reversed — funds flow back to the merchant (minus the chargeback fee, which is rarely refunded). If the evidence is weak or doesn't match the reason code, the chargeback stands.

This review typically takes 30 to 75 days depending on the network.

Step 8 — Pre-arbitration and arbitration (rare)

If the issuer rules in the merchant's favor but the cardholder pushes back again, the case can escalate to pre-arbitration and then to arbitration, where the card network itself decides. Arbitration is expensive — fees range from $250 to $500 per case regardless of who wins — and is uncommon for typical ecommerce disputes. Most cases end at Step 7.

How long does a chargeback take?

End to end, a chargeback usually resolves in 30 to 90 days. Here's a typical timeline:

- Day 0 — Customer files dispute with their bank.

- Day 1–3 — Bank provisionally credits the customer.

- Day 3–10 — Merchant is notified and funds are debited.

- Day 10–40 — Merchant gathers evidence and submits representment (deadline depends on network and reason code).

- Day 40–90 — Issuing bank reviews and rules.

- Day 90+ — Optional escalation to pre-arbitration or arbitration.

The customer can typically file a chargeback up to 120 days after the original transaction (Visa and Mastercard) — and in some reason codes, up to 540 days. That means a purchase from six months ago can still surface as a dispute today.

What does a chargeback cost a merchant?

The headline number is the disputed transaction amount plus the chargeback fee — but the real cost is much higher. For a typical $100 ecommerce order, a lost chargeback in 2026 costs the merchant:

- $100 — the disputed transaction amount (clawed back).

- $15–$100 — chargeback fee from the processor (Stripe charges $15; high-risk processors charge more).

- $25–$80 — the cost of goods, since the customer usually keeps the product.

- $20–$100 — marketing spend used to acquire the customer in the first place.

- $5–$15 — shipping, fulfillment, and payment processing fees that aren't refunded.

- Time — 30 to 60 minutes of staff time per dispute if handled manually.

Across the order, the true loss is typically 2 to 3 times the order value. And there's a compounding cost: processors track each merchant's chargeback ratio (disputes ÷ transactions). Crossing 0.9% on Visa or 1.0% on Mastercard pushes the merchant into a monitoring program with monthly fines, higher reserves, and — in severe cases — termination of the merchant account.

What's a "good" chargeback win rate?

Without automation, the average ecommerce merchant wins 20–30% of represented disputes. The remaining 70–80% either don't get fought (because the merchant misses the deadline or can't assemble the evidence in time) or are submitted with evidence that doesn't match the reason code.

With well-structured evidence packets and reason-code-specific rebuttal letters, win rates climb to 60–75%. AI-assisted dispute platforms reach this range by automatically gathering shipping, AVS, IP, and communication evidence the moment a dispute lands and drafting a rebuttal letter tuned to the specific reason code — work that's tedious for humans but easy to template.

How to win more chargebacks

A few principles separate merchants who win 60%+ from those who lose by default:

- Respond to every dispute, even small ones. Issuers and networks track merchant response rates. Ignoring disputes signals you can't defend them and worsens future outcomes.

- Match evidence to the reason code. Generic evidence packs lose. A "product not received" dispute needs tracking and delivery proof; an "unauthorized transaction" dispute needs AVS/CVV match, IP, and account history. Submitting the wrong evidence is the most common reason merchants lose disputes they should have won.

- Submit before the deadline, not on it. Issuers don't owe you a grace period. Late submissions are auto-lost.

- Use clear, formatted rebuttal letters. A short letter that cites the reason code, lists the evidence by exhibit number, and explains why each exhibit refutes the claim consistently outperforms a wall of unformatted text.

- Prevent disputes upstream. Clear billing descriptors, easy-to-find contact information, fast refunds, and proactive shipping updates eliminate a huge share of friendly-fraud chargebacks before they happen.

Frequently asked questions

Can you reverse a chargeback once it's filed? Yes — that's exactly what representment does. If the merchant submits evidence that satisfies the issuing bank, the funds (minus the fee) return to the merchant. The customer's provisional credit is reversed.

Are chargebacks the same as refunds? No. A **refund** is initiated by the merchant directly and costs only the order value. A **chargeback** is initiated through the bank, adds a fee, counts against your chargeback ratio, and can lead to processor penalties if it happens too often.

How long does a customer have to file a chargeback? Most reason codes allow **up to 120 days** from the transaction date for Visa and Mastercard, with some reason codes extending to 540 days. American Express and Discover have similar windows.

What's the difference between a chargeback and friendly fraud? A chargeback is the mechanism (a bank-initiated payment reversal). **Friendly fraud** is one type of chargeback — when a legitimate buyer files a chargeback for a purchase they actually made, usually instead of requesting a refund. Friendly fraud is the single largest category of disputes in ecommerce today.

Do you get the chargeback fee back if you win? Usually no. Most processors keep the chargeback fee even when the merchant wins the representment. A few processors refund the fee on a successful win — check your processor's policy.

How many chargebacks can a merchant have before getting in trouble? Visa flags merchants at a **0.9%** chargeback ratio; Mastercard flags at **1.0%**. Crossing those thresholds triggers a monitoring program with monthly fines, increased reserves, and potential termination of the merchant account. Most processors will alert you well before you hit the cap.

The bottom line

A chargeback is a structured, deadline-driven process — not a one-off event. The bank pulls the money, you have a short window to respond with evidence matched to the reason code, and the issuer decides. Merchants who treat disputes as a workflow, gather evidence systematically, and respond to every case win two to three times more often than merchants who don't.

RecovraFlow automates the evidence-gathering, deadline-tracking, and rebuttal-letter parts of that workflow so merchants can fight every dispute without hiring a dispute team. If you're losing more than a handful of disputes a month, the math of automation usually pays for itself in the first month.